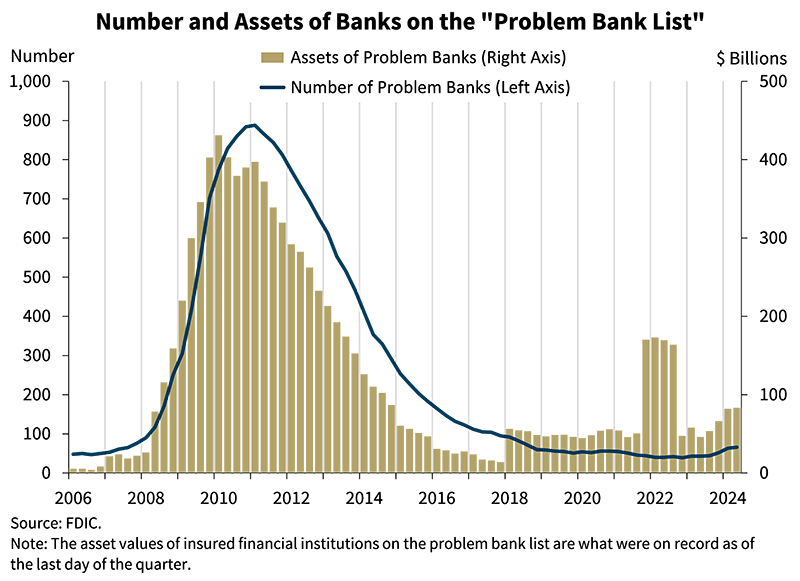

The variety of US banks with main points is on the rise, in response to the Federal Deposit Insurance coverage Company (FDIC).

The company’s Second Quarter 2024 Quarterly Banking Profile shows the variety of lenders on its “Drawback Financial institution Checklist” rose quarter-on-quarter from 63 to 66.

It’s the fifth consecutive quarterly improve of banks rated 4 or 5 on the CAMELS rankings system because the second quarter of 2023.

A score of 4 on the CAMELS system signifies a financial institution is affected by monetary, operational or managerial points that would moderately threaten viability if unresolved, whereas a score of 5 signifies a financial institution is critically poor and requires instant remedial consideration.

“The variety of drawback banks characterize 1.5% of whole banks, which is throughout the regular vary for non-crisis intervals of 1% to 2% of all banks. Complete property held by drawback banks elevated $1.3 billion to $83.4 billion.”

In the meantime, US banks proceed to saddle billions of {dollars} in unrealized losses on securities. The FDIC experiences $512.9 billion in whole unrealized losses within the second quarter, a 0.7% quarter-on-quarter lower.

Says FDIC chairman Martin Gruenberg,

“Rates of interest elevated modestly within the second quarter, placing downward strain on bond costs, however the ensuing improve in unrealized losses was greater than offset by the sale of bonds by a number of giant banks that resulted in substantial realized losses.

That is the tenth straight quarter that the trade has reported unusually excessive unrealized losses because the Federal Reserve started to lift rates of interest in first quarter 2022.”

The risks of unrealized losses got here into focus final yr amid the collapse of Silicon Valley Financial institution, when issues concerning the lender’s steadiness sheet triggered a financial institution run.

Immediately, Gruenberg says the US banking trade continues to display resilience, however dangers stay.

“…The trade nonetheless faces vital draw back dangers from uncertainty within the financial outlook, market rates of interest, and geopolitical occasions. These points may trigger credit score high quality, earnings, and liquidity challenges for the trade.

As well as, weak point in sure mortgage portfolios, notably workplace properties, bank cards, and multifamily loans, continues to warrant monitoring. These points, along with funding and margin pressures, will stay issues of ongoing supervisory consideration by the FDIC.”

Do not Miss a Beat – Subscribe to get e mail alerts delivered on to your inbox

Test Price Action

Observe us on X, Facebook and Telegram

Surf The Daily Hodl Mix

Disclaimer: Opinions expressed at The Day by day Hodl will not be funding recommendation. Traders ought to do their due diligence earlier than making any high-risk investments in Bitcoin, cryptocurrency or digital property. Please be suggested that your transfers and trades are at your individual threat, and any losses chances are you’ll incur are your accountability. The Day by day Hodl doesn’t suggest the shopping for or promoting of any cryptocurrencies or digital property, neither is The Day by day Hodl an funding advisor. Please notice that The Day by day Hodl participates in online marketing.

Generated Picture: Midjourney

{kind=link}